Introduction

Gold has long been considered a safe haven asset and a hedge against inflation, making it an attractive investment option for many UK investors. However, like most investments, profits from selling gold may be subject to Capital Gains Tax (CGT). This article explores the current CGT rules applicable to gold investments in the UK, helping investors understand their tax obligations and potential strategies to minimize their tax liability.

What is Capital Gains Tax?

Capital Gains Tax (CGT) is a tax paid on the profit when you sell, give away, or otherwise dispose of an asset that has increased in value. It is applicable to a wide range of assets including a second home, antiques, shares, or bullion.

Key points to understand about CGT:

- It only applies to the profit you’ve made, calculated as the difference between the purchase price and the sales price. For example, if you bought gold for £5,000 and sold it for £8,000, CGT would only apply to the £3,000 profit, not the full sale amount.

- CGT is payable if you make over a certain amount of profit from your bullion in a financial year.

Current CGT Allowance and Rates for 2024/2025

Each individual has an annual tax-free CGT allowance. For the tax year 2024-25, the annual exemption amount for Capital Gains Tax has been reduced to £3,000. This is the amount of profit you can make from your assets in this tax year before any tax is payable.

The tax rates that apply to gains over the allowance depend on your income tax band:

- The tax rate that you will pay varies from 18% to 24% – you can find the exact rate from the HM Revenue & Customs website.

CGT on Different Types of Gold Investments

Not all gold investments are treated equally for tax purposes. The CGT treatment depends on the form of gold you own:

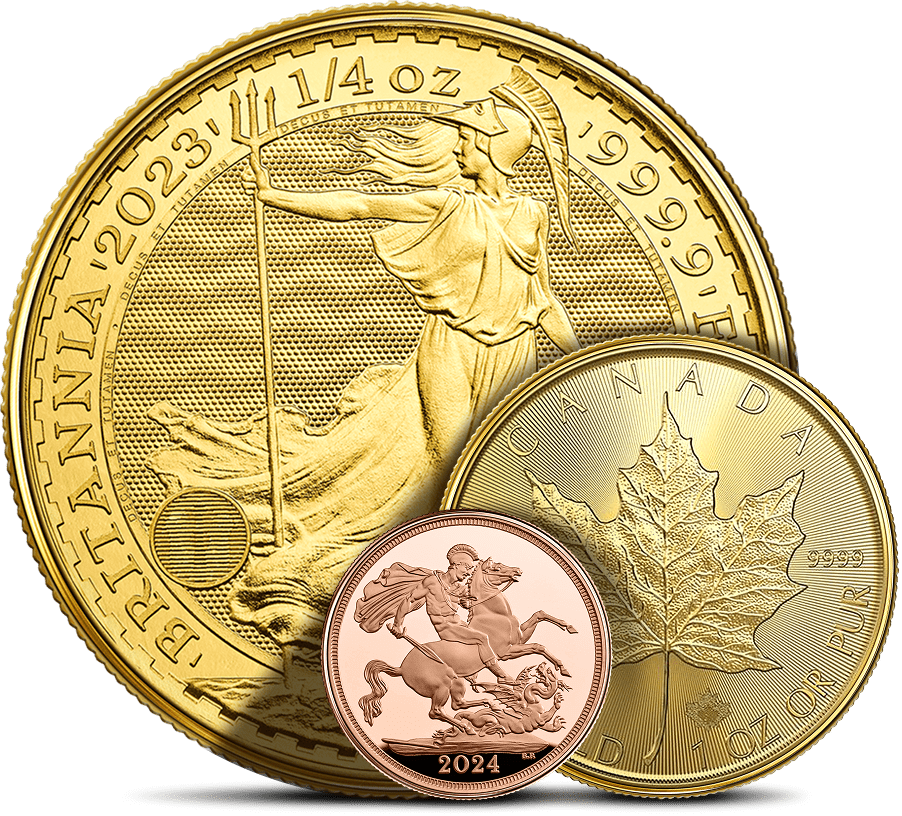

Gold Bullion Coins

Capital Gain Tax is exempt on all British legal currency. Therefore, gold Britannia coins, gold Sovereigns and other coins made by The Royal Mint, such as the Tudor Beasts and Royal Arms coins are all CGT exempt.

Bullion coins from The Royal Mint are exempt from Capital Gains Tax for UK residents due to their status as legal British currency. In fact, all gold, silver and platinum bullion coins produced by The Royal Mint are classed as CGT-free investments.

All profit realised on these investments, regardless of quantity or value, is tax-free.

Under HMRC rules all British legal currency coins are exempt from Capital Gains Tax. This includes gold Britannia coins, silver Britannia coins and gold Sovereigns (from 1837 onwards) just to name a few.

A brief list of CGT-exempt gold coins includes:

- Gold Britannia coins

- Gold Sovereigns (post-1837)

- Gold Half Sovereigns

- Queen’s Beasts coins

- Tudor Beasts coins

Gold Bullion Bars

Unlike certain coins, gold bars are subject to CGT:

Gold bars are not exempt from capital gains tax and if an investor has used all their capital gains tax free allowance, then capital gains tax will apply.

All gold and silver bullion bars are taxable with CGT, so this can be an important consideration for large investors.

Foreign Gold Coins

Coins which are currency but not sterling, for example Krugerrands, are chargeable assets. This means that non-UK coins like American Eagles, Canadian Maple Leafs, or South African Krugerrands would be subject to CGT on any profits over the annual allowance.

Strategies to Minimize CGT on Gold Investments

There are several legitimate strategies that investors can employ to minimize their CGT liability:

1. Invest in CGT-Exempt Coins

The simplest way to avoid paying CGT on your gold investments is to invest in British gold bullion coins manufactured by The Royal Mint. These include the gold Britannia coins or Sovereigns. Because these coins are considered legal British currency, they are not subject to CGT which means investors can earn unlimited tax-free profits upon sale.

2. Utilize Your Annual CGT Allowance

If your gold investments are liable for CGT, you may consider spreading your sales over multiple financial years to stay within the annual CGT allowance. For example, if you bought £14,000 worth of gold in 2012 and they’re worth £20,000 in 2024, you would be selling them at a profit of £6,000. Instead of selling them and realising that profit right away, you could sell half the gold investments in the current financial year and the remainder in the next.

3. Offset Losses Against Gains

Losses from gold and silver investments can be used to offset other capital gains, potentially reducing your taxes. You can use up to £3,000 of the excess loss to offset other income if your losses exceed your gains. Any remaining loss can be carried forward to future years.

Practical Example: The Tax Savings from Investing in CGT-Exempt Coins

To help highlight the potential benefits of buying British gold coins, a gold investment of £50,000 in September 2007 would be worth over £150,000 in November 2011. If this gold investment was made in any way other than British gold coins the gain would be liable to Capital Gains Tax. Therefore the tax saving to a CGT paying individual looking to realise this investment would be up to £28,000.

Self-Assessment and Reporting Requirements

CGT is a self-assessed tax in the UK:

In the UK, CGT is a self-assessed tax. This means it’s up to each individual investor to declare and pay any capital gains tax they owe.

Staying on top of filing deadlines is critical to avoid unnecessary penalties: Self-Assessment Tax Return Deadline: 31 January 2025 (for the 2023/24 tax year).

Conclusion

Understanding the CGT implications of your gold investments is crucial for effective tax planning. By choosing CGT-exempt British legal tender coins, strategically timing your sales, and properly utilizing your annual allowance, you can significantly reduce or even eliminate your tax liability on gold investments.

For large investors or those with complex investment portfolios, seeking professional advice from a qualified financial advisor or tax specialist is recommended to ensure compliance with all tax obligations while maximizing after-tax returns.

Disclaimer: While this article aims to provide accurate and up-to-date information, tax laws and rates are subject to change. This article should not be considered as financial or tax advice. Always consult with a qualified tax professional for advice specific to your situation.